Understanding the PPP Project Lifecycle: From Initiation to Handover

What Is a PPP and Why Does the Lifecycle Matter?

A Public-Private Partnership (PPP) is a long-term contractual arrangement between a government body and a private party to deliver public infrastructure or services, where the private sector takes on significant responsibility — and risk — in exchange for revenue over time. Crucially, this is not privatisation: the public sector retains strategic ownership and accountability for the underlying service.

The structured lifecycle matters because PPP projects are not one-off transactions. They typically span 20 to 35 years across multiple distinct phases, each with its own decision points, obligations, and risk profile. A procurement team that understands only the bidding phase will be unprepared for the contract management demands that follow financial close. Equally, a contracting authority that loses focus after construction completion may find itself with a deteriorating asset and no leverage at handover.

Whether you are evaluating a tender, preparing a bid, or managing an active concession, the lifecycle framework gives you a map of where you are, what decisions are approaching, and who bears responsibility at each turn.

Phase 1 — Project Identification and Feasibility

The lifecycle begins when a contracting authority — typically a government ministry, agency, or municipality — identifies a candidate project and tests whether the PPP route is genuinely appropriate. This phase is more analytical than many participants expect.

Early work includes technical feasibility studies, demand projections, and an initial cost estimate. The critical analytical tool here is the Value for Money (VfM) assessment, which compares the expected whole-life cost of a PPP against a Public Sector Comparator — a modelled estimate of what traditional procurement would cost, adjusted for risk retention. If the PPP route does not demonstrate a credible VfM advantage, the project should not proceed on that basis.

Getting the feasibility phase right has downstream consequences that are hard to reverse. Optimism bias in demand forecasting, for instance, regularly distorts VfM conclusions and leads to renegotiation years later. The World Bank and OECD both publish guidance frameworks for VfM methodology that contracting authorities can reference when structuring this analysis.

By the end of Phase 1, the authority should have a project that is technically viable, legally permissible, and demonstrably better suited to PPP delivery than conventional procurement.

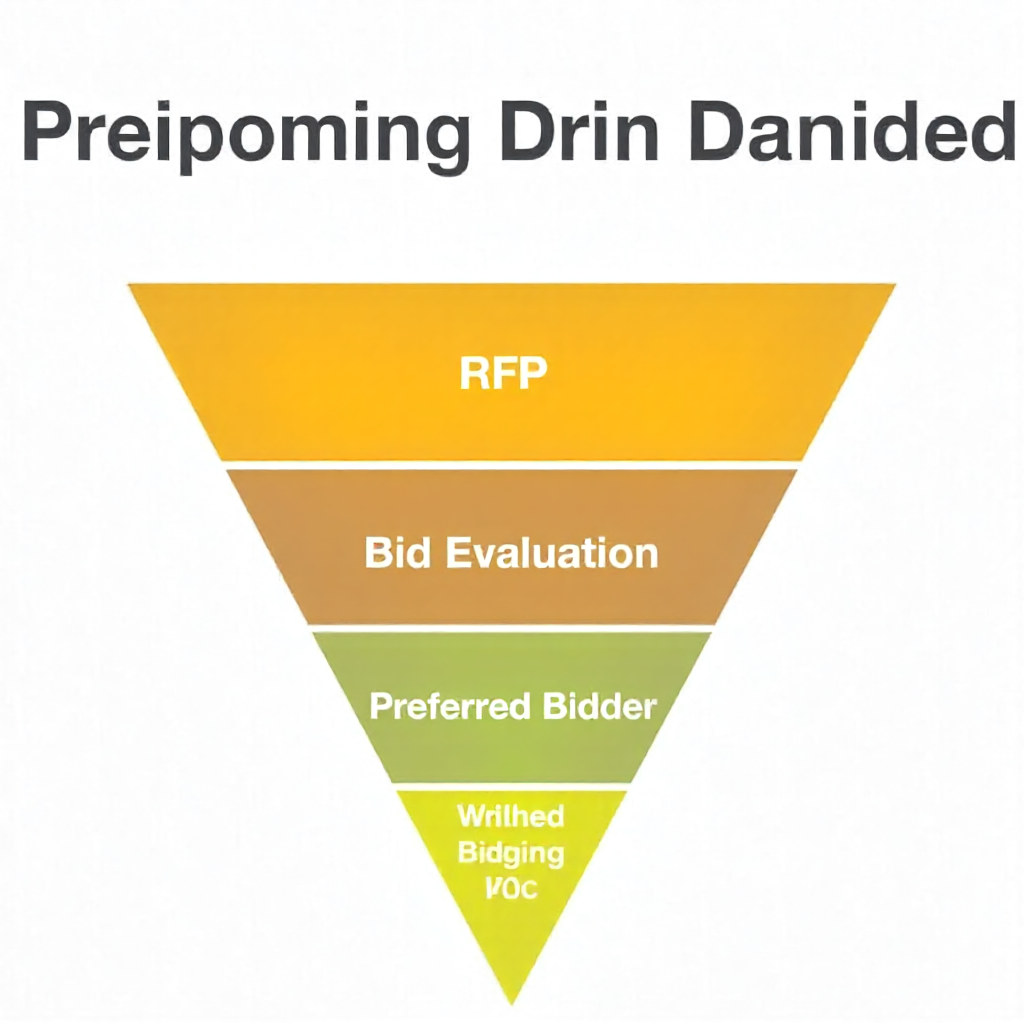

Phase 2 — Structuring and Procurement

The procurement phase is where the commercial architecture of the project takes shape. The contracting authority prepares tender documents, issues a Request for Proposals (RFP), evaluates bids, and selects a preferred bidder — but the work behind that sequence is substantial.

Risk allocation is the central design question at this stage. The governing principle is straightforward: each risk should be assigned to the party best placed to manage it. Construction risk typically sits with the private partner. Regulatory or political risk usually stays with the public sector. Demand risk can go either way depending on the project type — a toll road handles it very differently from a hospital.

Bid evaluation criteria must be established before the RFP is issued, covering technical capability, financial robustness, proposed service delivery model, and price. Evaluation panels that change their weighting criteria mid-process invite legal challenge and delay.

The procurement phase closes when a preferred bidder is formally notified and enters the period of exclusive negotiation leading toward financial close. That gap — often three to nine months — is where many projects stall or unravel.

Phase 3 — Financial Close and Contract Execution

Financial close is the point at which all financing agreements are signed, equity is committed, and the project company can begin drawing funds to start construction. It is distinct from contract signing, which can occur weeks or months earlier.

Between preferred bidder selection and financial close, the private partner typically establishes a Special Purpose Vehicle (SPV) — a legally ring-fenced project company that holds the concession, raises debt, employs contractors, and manages the asset. The SPV structure protects the parent companies from unlimited liability while giving lenders a clearly defined security package.

Financing arrangements at this stage usually combine senior debt from commercial banks or development finance institutions, mezzanine finance, and equity from the sponsors. Lenders will conduct their own due diligence and require a direct agreement with the contracting authority — often called a step-in right — that allows them to cure a contractor default before the concession is terminated.

The concession agreement is executed at or around financial close. This document governs the entire relationship between the contracting authority and the SPV for the life of the project. Its drafting quality directly affects how smoothly — or contentiously — the next 25 years will run.

Phase 4 — Construction and Development

Once financial close is reached, the construction phase begins and the private partner takes the operational lead. The SPV's engineering, procurement, and construction (EPC) contractor is responsible for delivering the asset on time, within budget, and to the agreed specification.

The contracting authority's role shifts to monitoring rather than managing. Independent certifiers or technical advisers are commonly appointed to verify that construction milestones have been met before payments are released. This is where the payment mechanism design — established in the concession agreement — becomes operational.

PPP projects typically use either availability-based payments (where the authority pays when the asset is available and performing) or demand-based revenue (where the private partner collects user charges). In availability models, no payment is triggered until the asset is handed over and certified as operational — creating a strong financial incentive for on-time completion.

Delays during construction are more than a scheduling problem. In a leveraged SPV, every month of delay increases interest during construction and compresses the revenue period. Contractors absorb this risk through liquidated damages provisions, but prolonged disputes over delay liability can consume management time across both sides for years.

Phase 5 — Operations, Maintenance, and Performance Management

The operational phase is the longest and, in revenue terms, the most significant part of the lifecycle. Operations and maintenance (O&M) obligations typically run for 20 to 30 years and are tightly governed by a KPI framework embedded in the concession agreement.

Performance is measured through a deduction mechanism: if the SPV fails to meet defined service standards — response times, availability percentages, quality thresholds — the authority applies financial deductions to the periodic payment. These are not penalties in the punitive sense; they are calibrated reductions that reflect the reduced value of the service delivered.

Contract management on the authority's side requires dedicated resource. A common failure mode is the contracting authority allowing its PPP contract management unit to atrophy after construction, only to find years later that it has lost the institutional knowledge needed to apply deductions correctly, process change requests, or prepare for handover.

Lifecycle maintenance planning is also critical here. The concession agreement should require the SPV to maintain a lifecycle maintenance reserve — a fund set aside to cover major asset renewals (roof replacements, HVAC systems, structural works) that fall due at predictable intervals. Authorities that do not monitor this reserve risk inheriting an asset that is technically operational but commercially exhausted at handover.

Phase 6 — Handover and Post-Concession Transition

Asset reversion to the public sector at the end of the concession is the most commercially underestimated phase of the entire lifecycle. The contracting authority regains full ownership and operational responsibility — and the condition in which it receives the asset depends entirely on how well handover provisions were drafted and enforced years earlier.

Handover requirements typically include a condition survey conducted 2 to 5 years before expiry, residual asset life requirements (specifying that major components must have a defined remaining service life), and knowledge transfer obligations covering maintenance records, as-built drawings, and operational manuals.

Where the asset falls short of the required condition standard, the SPV is obliged to carry out remediation works or pay a financial equivalent into an escrow account. In practice, the negotiation of handover condition can be contentious — the SPV's incentive to invest declines as the concession approaches expiry, which is why proactive contract management in the final five years matters so much.

Authorities preparing for reversion should begin workforce planning well in advance. In-house O&M capacity or a new service provider needs to be in place at the moment the concession ends, with no gap in service delivery.

Frequently Asked Questions

What is the typical duration of a PPP project lifecycle?

Most PPP concessions run between 20 and 35 years in total, covering construction and the full operational period. Social infrastructure projects (schools, hospitals) often sit at the shorter end; transport concessions (roads, rail, ports) frequently extend to 30 years or beyond. The duration is driven by the time needed to amortise the private investment and generate an acceptable return.

Who is responsible for managing a PPP contract once it is operational?

Contract management responsibility sits with the contracting authority, usually through a dedicated PPP unit or contract management team. The SPV manages day-to-day operations, but the authority remains accountable for monitoring performance, processing change requests, applying the payment mechanism, and preparing for eventual handover.

What happens if a private partner fails to meet performance targets during the operational phase?

Persistent underperformance triggers a graduated response under the concession agreement. Initial failures result in financial deductions. Continued non-performance can escalate to warning notices, step-in rights for the authority or lenders, and ultimately termination for cause — though termination is rare and expensive for all parties. Most contracts are designed to incentivise correction before reaching that threshold.

How does financial close differ from contract signing?

Contract signing is when the concession agreement is executed between the contracting authority and the SPV. Financial close is when all financing documents are signed and the project company can draw funds. The two events are related but separate — financial close typically follows contract signing by weeks or months, and a project can be contractually committed but not yet funded during that interval.

Can a PPP concession be terminated early, and what are the consequences?

Yes, early termination is possible under three scenarios: termination for SPV default, termination for authority default, and termination for convenience (where the authority chooses to exit). Each triggers a different compensation formula. Termination for authority default or convenience generally requires the authority to pay outstanding debt and a proportion of equity value. Termination for SPV default may result in a much lower — or zero — compensation payment, depending on the contract structure and jurisdiction.